The average American household spent $77,280 in 2023 according to the Bureau of Labor Statistics Consumer Expenditure Survey. The personal savings rate during that same year hovered below 4%. That gap between what households earn and what they actually keep is exactly where frugal living becomes valuable.

Most people who try cutting expenses quit within two months. Not because frugal living is hard, but because they start with the wrong strategy. They eliminate daily coffee and cancel one streaming service, watch their savings account barely move, and conclude that frugal living is not worth the effort. The strategy failed, not the person.

The frugal living tips in this guide take a different approach. Every major spending category gets its own section: food, housing, transportation, entertainment, and budgeting. More importantly, each section starts with the highest-impact actions first, so your effort goes toward what actually changes your financial picture. If you want to go deeper on any individual tactic, 50 frugal living tips that save money every month expands on each category with additional specific strategies you can apply immediately.

What Is Frugal Living? (And What It Definitely Isn’t)

The Real Definition of Frugal Living

Frugal living is the practice of intentionally directing money toward what genuinely matters to you by eliminating or reducing spending on what does not. It is a strategy built on value, not deprivation. Frugal people spend confidently on their real priorities and cut everything else without apology or guilt.

This definition matters because it separates frugal living from the miserable version of “spend nothing” that most people imagine and reject. A frugal person is not someone who refuses to buy anything. A frugal person is someone who has decided, with clarity and intention, what their money is actually for, and refuses to spend it on things that fall outside that definition.

The Latin root of “frugal” is frugalis, meaning economical and worthy of value. The modern practice carries that same core idea: frugality is about maximizing value per dollar, not minimizing dollars spent. A frugal person will pay more for a quality winter coat that lasts fifteen years than for a cheap one replaced every two seasons. That same person will refuse to pay for a gym membership they use twice a month when their neighborhood has three parks and a free public recreation center.

Frugal living works best when it begins with a clear picture of your own priorities, not someone else’s. What you cut and what you protect will differ from any other household. The framework is universal; the application is personal.

Frugal vs. Cheap: Why the Difference Matters

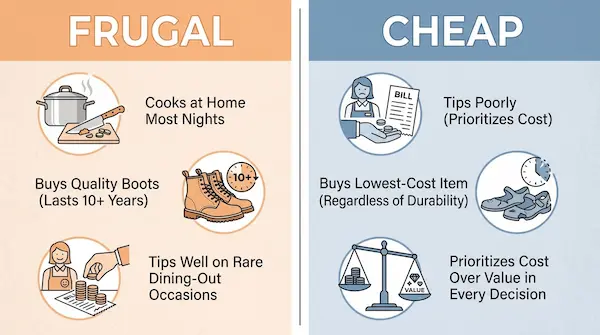

Cheap and frugal are not synonyms, and conflating them is one of the main reasons people resist adopting frugal habits.

A cheap person minimizes cost at the expense of quality, relationships, or long-term outcomes. A frugal person minimizes waste while maximizing genuine value. The behavioral difference shows up in small but meaningful ways. A cheap person tips poorly at a restaurant they chose to visit. A frugal person cooks at home most nights, then tips generously on the rare occasion they go out. A cheap person buys the lowest-cost version of everything regardless of how long it will last. A frugal person researches the best value per dollar, which sometimes means paying a higher upfront price for something that holds up for years.

The distinction matters for two practical reasons. First, it changes how frugal living feels to practice day to day. People operating from a value framework make deliberate choices and feel good about them. People operating from a pure cost-minimization framework feel constantly deprived and usually quit. Second, it changes how people around you experience your habits. Friends and family who observe genuine generosity alongside strategic cost-cutting accept and often admire frugal behavior. Those who observe universal cheapness often pull away.

Internalizing the frugal-versus-cheap distinction makes the difference between frugal living as a sustainable long-term lifestyle and frugal living as a two-month experiment that fails.

Why These Frugal Living Tips Work When Others Don’t

Most frugal living content treats every saving strategy as equally valuable. A tip about turning off lights when you leave a room appears alongside a tip about renegotiating your rent, as if both deliver equivalent results. They do not. The difference between a strategy that produces visible financial improvement and one that produces mostly effort comes down to where in your budget you apply your attention.

The 80/20 Rule Applied to Personal Finance

The Pareto Principle holds that roughly 80% of outcomes come from 20% of causes. In personal finance, this plays out with remarkable consistency. Housing, transportation, and food together account for approximately 63% of average American household spending according to BLS Consumer Expenditure Survey data. Optimizing these three categories delivers more financial impact than any combination of micro-saving tactics applied to everything else.

This is the strategic error embedded in most frugal living guides. They bury the highest-impact strategies alongside dozens of low-impact suggestions without ever telling the reader which actions matter most. Unplugging phone chargers when not in use saves approximately $1.00 per month. Renegotiating a car insurance policy saves an average of $568 per year according to Bankrate’s auto insurance research. Both are “frugal living tips.” Only one meaningfully changes your financial situation.

Spend the first 90 days of any frugal living effort focused entirely on the three largest categories in your own budget, and you will achieve more than a year of scattered small cuts. Identify those three categories by reviewing three months of bank and credit card statements before you change a single behavior.

AUTHOR NOTE: After reviewing spending patterns across dozens of households, the pattern is consistent: people who start by attacking small expenses stay motivated for about three weeks before giving up when their savings barely move. People who address a single major expense first, even imperfectly, see a tangible result that gives them the confidence to continue. The order in which you tackle your spending matters as much as which tactics you use.

How Small Daily Savings Compound Into Real Wealth

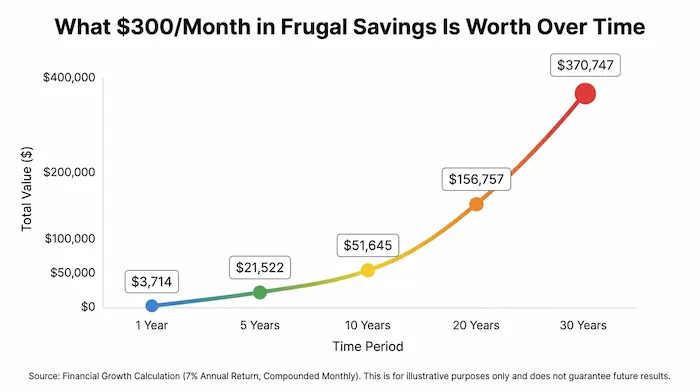

The frugal living math that most content leaves out is what consistent savings are actually worth over time. A modest monthly reduction of $300, invested in a broad-market index fund at a 7% average annual return, produces the following outcomes:

| Timeframe | Monthly Amount Invested | Total Accumulated (7% Annual Return) |

| 1 year | $300 | $3,731 |

| 5 years | $300 | $21,537 |

| 10 years | $300 | $52,068 |

| 20 years | $300 | $157,413 |

| 30 years | $300 | $378,684 |

The strategies across every category in this guide, applied consistently, can realistically reduce monthly spending by $300 to $800 depending on your current habits and income level. At $500 per month, the 30-year compound figure exceeds $600,000. The individual actions are modest. The long-term financial consequence is not.

PRO INSIGHT: Behavioral economics research published through the National Bureau of Economic Research consistently demonstrates that people dramatically underestimate the value of small, repeated financial decisions because the human brain is poorly calibrated for evaluating compound effects over long time horizons. The reason frugal living produces outsized results over a lifetime is not that any individual saving is large. It is that each frugal decision is a permanent behavior change applied to hundreds of future purchase moments.

Frugal Living Tips for Food and Groceries

Food is the third-largest household expense for most American families. The USDA’s Food Plans: Cost of Food reports estimate that a family of four following a moderate-cost plan spends approximately $1,000 to $1,200 per month on food, with higher-spending households reaching $1,500 or more. Unlike a fixed mortgage payment or car loan, food spending can be adjusted daily. That flexibility makes groceries both the easiest category to start with and one of the highest-return targets in any frugal living effort.

How to Meal Plan and Cut Your Grocery Bill in Half

Meal planning is the single highest-return food strategy available to most households. The mechanism is straightforward: when you know exactly what you need before entering a store, you buy exactly what you need. Impulse purchases disappear. Food waste drops sharply. And you stop buying groceries you later throw away.

Here is a meal planning system that works without requiring hours of preparation:

- Select four to five dinners for the upcoming week, not seven. Plan two nights of leftovers or flexible meals using whatever needs to be used up.

- Write your grocery list directly from those specific recipes before opening any shopping app or setting foot in a store.

- Check your pantry, freezer, and refrigerator before writing the list. Most households have 30–40% of an upcoming week’s meals already on hand.

- Shop once per week. Each additional store trip adds an estimated $20–$30 in unplanned purchases.

- Note unit prices (price per ounce or per serving) when comparing products. Store-brand items are often nutritionally identical to name brands at 20–40% lower cost.

Meal planning reduces grocery spending not by being restrictive but by replacing unplanned decisions with planned ones. Unplanned decisions at 6 PM on a Tuesday are expensive: takeout, overpriced grab-and-go items, and grocery runs where you buy whatever looks good. Planned decisions made on Sunday morning are economical.

For those beginning their frugal journey from scratch, frugal living tips for beginners: how to start saving money today walks through a complete first-month meal planning approach, including a sample weekly template and a starter pantry list.

Smart Shopping Habits That Save Money Without Couponing

Traditional couponing works for a narrow set of highly motivated people. For most households, it is a system that trades three to four hours per week for $15–$25 in savings, often on products you would not have purchased at full price. The math frequently does not favor the effort.

The more effective alternative combines three high-impact habits. First, shop loss leaders: most major grocery chains deeply discount specific items each week to drive foot traffic. These items, particularly shelf-stable goods like pasta, canned tomatoes, cooking oils, and spices, are worth buying in quantity when on sale. Second, maintain a price book. This does not have to be elaborate. Note the regular price and unit price of the 20 items you buy most frequently. When you see a genuine sale versus an inflated “sale” price, you will know instantly. Third, choose your store based on your actual shopping list rather than habit or convenience. The price difference between a budget grocery chain and a premium grocer for an identical basket of staple goods can reach $100 per month for a family of four.

PRO INSIGHT: The single most impactful food savings opportunity most households overlook is reducing waste before adding any other strategy. The USDA Economic Research Service estimates that American households waste between 31–40% of the food supply. For a household spending $800 per month on groceries, that represents $250–$320 thrown in the trash every month. A two-week waste audit (tracking what gets thrown out and why) before implementing any other grocery strategy often reveals more savings opportunity than any combination of couponing and meal planning.

Frugal Living Tips for Housing and Utilities

Housing is the largest single expense for most American households, consuming approximately 33% of total annual spending according to the Bureau of Labor Statistics. Reducing housing costs directly (negotiating rent, refinancing a mortgage, downsizing, or house hacking) produces the highest financial impact of any category but also carries the highest friction and life disruption. Utility and maintenance costs offer meaningful savings with far less upheaval, and they compound over years of consistent application.

Reducing Monthly Utility Costs Without Discomfort

Utility costs respond to behavioral adjustments more predictably than almost any other household expense. The most effective strategies, ordered by annual impact:

Heating and cooling account for the largest share of most home energy bills. A programmable or smart thermostat, set to reduce heating and cooling during sleeping hours and unoccupied periods, can reduce annual energy costs by 10–15% according to the U.S. Department of Energy. For a household spending $200 per month on energy, that is $240–$360 in annual savings from a single behavioral adjustment requiring minimal ongoing effort.

Water costs respond quickly to low-effort interventions: low-flow showerheads, prompt faucet leak repairs, and running dishwashers and washing machines only when full can reduce water bills by 15–20% in most households.

Internet and phone bills are among the most consistently under-renegotiated household expenses. Most providers offer retention discounts to customers who call and express intent to switch. A 20-minute phone call to your current provider asking for a better rate, or a quick comparison through a competing provider’s website, frequently yields $20–$40 per month in immediate savings. Many households have not renegotiated these contracts in three or more years and are paying above current market rates without knowing it.

DIY Maintenance and Repair That Protects Your Budget

Home maintenance is where frugal living and genuine financial protection intersect. Deferred maintenance is one of the most expensive financial mistakes a household can make: a $12 tube of caulk applied to a window frame today can prevent a $400 mold remediation bill the following year. Replacing a worn wax ring on a toilet for $8 in materials and 45 minutes of effort is the same repair that costs $150–$200 when a plumber makes the call.

Learning to handle basic home repairs independently is a high-return skill investment that pays dividends for decades. Most homeowners and renters significantly overpay for minor repairs simply because they have never attempted them. Tasks including unclogging drains, patching small drywall holes, replacing faucet washers, weatherstripping doors, and repainting trim require $15–$30 in materials, 1–3 hours of time, and a YouTube tutorial. Hired out, those same repairs typically cost $100–$300 each.

Renters benefit equally from this mindset. Understanding how to identify and document maintenance issues, communicate them to landlords clearly and promptly, and handle the minor repairs a lease permits you to address independently reduces both lease penalties and unnecessary wait times for professional repairs.

Frugal Living Tips for Transportation

Transportation is the second-largest household expense category for most American families, consuming approximately 16–17% of total annual spending. Unlike housing or food, transportation costs are distributed across multiple simultaneous decisions: vehicle purchase price, financing interest, insurance, fuel, maintenance, parking, tolls, and ride-shares each accrue independently. Most households actively manage one or two of these. Frugal living requires addressing all of them.

Cutting Car Ownership Costs Strategically

The full cost of car ownership spans six categories: purchase price and depreciation, financing interest, insurance, fuel, maintenance, and parking or tolls. Most people only consciously manage fuel and maybe insurance. The four they tend to ignore often cost more than the two they track.

Insurance is the most consistently underoptimized transportation expense in the average household budget. Comparison shopping for car insurance annually saves drivers significant amounts, with providers frequently offering substantially lower rates than what auto-renewing customers pay. Running a comparison through a broker or aggregator takes approximately 20 minutes and requires no change in coverage.

Fuel costs respond directly to driving behavior. Reducing highway speed from 75 mph to 65 mph improves fuel efficiency by roughly 10–15%. Consolidating errands into single trips, maintaining correct tire pressure, and using apps to locate the lowest nearby fuel price all reduce annual fuel costs meaningfully. None of these require any upfront investment.

Consistent preventive maintenance is where the frugal approach to transportation is most frequently misunderstood. Skipping oil changes, ignoring brake wear indicators, or deferring tire rotations to save $30–$50 in the short term creates the $800–$2,000 repairs that derail budgets entirely. Investing consistently in scheduled maintenance is frugal. Deferring it is not.

When Alternative Transportation Actually Saves You More

For households in moderate-density urban areas, the frugal calculation on car ownership itself deserves examination at least once every few years. AAA estimates the total annual cost of vehicle ownership (including depreciation, financing, insurance, fuel, maintenance, and fees) typically exceeds $10,000 per year for the average American driver. In cities with reliable public transit access, replacing a second vehicle with a combination of transit, cycling, and occasional ride-shares can save $5,000–$9,000 annually.

This is not a realistic option for every household. Rural and many suburban households need personal vehicles. But dual-vehicle households in mid-to-large cities who have not run a genuine total-cost comparison on their second vehicle are often surprised by the math.

Cycling deserves specific mention for shorter commutes. A quality commuter bicycle ($300–$700) paid for itself within one to two months compared to fuel and parking costs alone, has annual maintenance costs measured in tens of dollars rather than thousands, and produces a tangible improvement in daily physical activity as a side benefit.

Frugal Living Tips for Entertainment, Subscriptions, and Lifestyle

Lifestyle spending is where frugal living gets personal. Food, housing, and transportation have relatively clear optimization targets. Discretionary entertainment and lifestyle costs are tied directly to quality of life, social connection, and personal identity. Cutting them carelessly produces misery and almost always leads to abandonment. Cutting them strategically produces both meaningful savings and often a higher-quality version of the experiences you actually value.

The Subscription Audit: A Step-by-Step System

Research from West Monroe Partners found that consumers consistently underestimate their monthly subscription spending, often by more than $100 per month. Subscriptions accumulate silently: streaming services, software tools, app purchases, music platforms, fitness apps, cloud storage tiers, and news publications all charge small recurring amounts that add up to a surprising total.

The subscription audit is one of the fastest, highest-return frugal living actions available: it requires 30–45 minutes, produces immediate monthly savings, and requires no ongoing behavioral change after the initial session.

Run your subscription audit using these steps:

- Pull three months of bank statements and credit card statements. Every statement, every account.

- Highlight every recurring charge regardless of the amount. Anything that repeats monthly, quarterly, or annually qualifies.

- Create a list of each subscription, its monthly cost, and the last date you actively used it.

- Cancel immediately any subscription you have not used in the past 60 days. Do this before moving to step five.

- For subscriptions you actively use, identify which can be shared through family plans, downgraded to a lower tier, or replaced with a free alternative that delivers equivalent value.

- Set a quarterly calendar reminder to repeat this process. Subscriptions re-accumulate.

Most households identify $40–$100 per month in unused or redundant subscriptions during their first audit. For the entertainment subscriptions you choose to keep, rotating them by season rather than maintaining all simultaneously cuts costs by 50–70% without any loss of access to content.

Free and Low-Cost Alternatives That Don’t Feel Like Sacrifice

The frugal living trap in entertainment is assuming that free alternatives are inferior experiences. This assumption is both common and largely incorrect.

Public libraries have quietly become one of the most powerful frugal living resources in existence. A current library card provides access to digital books, audiobooks through apps like Libby and Overdrive, streaming services through platforms like Kanopy and Hoopla, museum passes in many cities, tool-lending libraries, and seed libraries for gardeners. The total monetary value of a library card used intentionally can exceed hundreds of dollars per month in equivalent paid services.

For social entertainment, the shift from going out to having people over is one of the most consistently high-satisfaction frugal substitutions available. A dinner party for four at home costs $50–$70 in food and produces an experience that most participants find more enjoyable and more memorable than the same group spending $200 at a restaurant. The frugal option is objectively better in almost every way except one: it requires planning and effort in advance.

For families navigating entertainment costs with children, frugal living tips for families on a tight budget covers school expenses, activity fees, family outings, and holiday spending with specific strategies calibrated for households with kids at different ages.

How to Build a Budget That Supports Frugal Living

Frugal living without a budget is navigation without a map. You may be making progress, but you have no way of measuring it, no clear destination, and no early warning system when spending drifts in the wrong direction. A budget gives every frugal strategy a context to operate within and a measurement against which you can track results over time.

Choosing the Right Budgeting Method for Your Personality

No single budgeting method works for every person, and the research on adherence is consistent: the best budget is the one you will actually maintain past month two. Three methods produce strong results for different personality types:

The 50/30/20 rule allocates 50% of after-tax income to needs (housing, food, utilities, transportation), 30% to wants, and 20% to savings and debt repayment. For frugal living, the goal over time is to reduce the needs allocation below 50% and redirect that margin into savings. This is the right starting framework for people new to budgeting because it requires minimal tracking and builds awareness before demanding precision.

Zero-based budgeting assigns every dollar of income a specific role before the month begins: savings, fixed bills, variable categories, everything receives an allocation. No dollar goes unassigned. This method produces the highest savings rates among people who follow it consistently because it eliminates the spending drift that accounts for most budget failures. It requires more setup time but very little daily management once the initial category allocations are established.

The cash envelope system assigns a physical cash envelope to each discretionary spending category: groceries, dining out, entertainment, clothing. When the envelope is empty, spending in that category stops until the next budgeting period. This method is particularly effective for people who struggle with abstract digital transactions because physically handing over cash creates psychological friction that tapping a debit card does not. The cash envelope system is the foundation of Dave Ramsey’s popular debt-elimination program for this reason.

Choosing a budgeting method is less important than choosing one and starting. Switching methods after 90 days of data is easy. Starting is the only decision that matters right now.

For a structured approach to launching a first budget and tracking your first full month of spending, extreme frugal living tips: 35 ways to cut expenses and save more includes a 30-day launch sequence designed for people starting from scratch.

Tracking Spending Without Micromanaging Every Dollar

The most common reason people abandon a budget after the first month is not lack of discipline. It is over-engineering. Tracking every transaction in a spreadsheet, updating it daily, categorizing it manually, and reconciling it weekly creates an administrative burden that most people will not sustain indefinitely alongside a real life.

The sustainable alternative is category-level tracking with a single weekly review. You maintain awareness of what you are spending in each major category (food, housing, transportation, entertainment, personal care), review those totals once per week for 10–15 minutes, and adjust the following week if any category ran significantly over. This approach catches budget drift early without creating a second job.

Apps like YNAB (You Need A Budget) and Copilot automate transaction import and categorization, reducing weekly review time to under 15 minutes. Many users report that the first two weeks of tracking produce spontaneous behavior change without any deliberate effort, simply because seeing real numbers attached to spending categories creates immediate awareness.

PRO INSIGHT: The category most people underestimate in their budget is not entertainment or dining out. It is irregular expenses: car registration, holiday gifts, medical copays, a broken phone screen, a last-minute travel expense. These feel surprising each time, but they are predictable in aggregate. Creating a dedicated “irregular expenses” sinking fund and contributing $50–$100 per month to it eliminates the budget-busting surprises that derail most households by month three. When the car registration comes due, you have the money. When it does not, the money grows toward the next irregular expense that will.

Frequently Asked Questions About Frugal Living Tips

What is frugal living?

Frugal living is a lifestyle approach that prioritizes intentional, value-focused spending over default consumer habits. Rather than spending based on impulse or social expectation, frugal individuals deliberately direct their money toward what genuinely matters to them while minimizing spending on what does not align with their values or goals. It is defined by intentionality, not deprivation or self-denial.

How do I start living frugally?

Start by tracking all spending for 30 days without changing any behavior. Once you have real data on where your money currently goes, identify the single largest spending category above your target and address it first. Most beginners see the fastest results starting with grocery spending, subscription services, or their largest utility bill, since all three respond immediately to straightforward behavioral changes.

How much money can you save by living frugally?

Results vary widely by income, current spending habits, and how consistently strategies are applied. Most households can realistically reduce monthly spending by $200–$600 through consistent application of strategies across the categories covered in this guide. At $300 per month invested at a 7% average return, that sum accumulates to over $52,000 in 10 years and over $378,000 in 30 years.

Is frugal living worth it?

Frugal living is worth it for anyone whose current spending leaves them financially stressed, unable to save meaningfully, or working toward a specific goal such as debt elimination, a home purchase, or early retirement. Evidence from the FIRE (Financial Independence, Retire Early) community demonstrates clearly that sustained frugal habits combined with higher savings rates can accelerate financial independence by 10–20 years compared to median American consumption patterns.

What is the difference between frugal and cheap?

Frugal means spending intentionally on genuine value and cutting spending on what delivers no real return. Cheap means minimizing cost regardless of quality, relationships, or long-term consequences. A frugal person pays for quality when the long-term value justifies it and cuts ruthlessly when it does not. A cheap person prioritizes the lowest price in every situation, which often creates higher costs over time through poor-quality products, strained relationships, and deferred expenses that become larger problems.

Conclusion

Frugal living is not about squeezing enjoyment out of your daily life. It is about refusing to let default spending patterns and consumer marketing decide what your money is for. The frugal living tips across this guide, applied systematically starting with your three highest-spending categories, can realistically redirect $300–$600 per month away from low-value spending and toward financial progress that compounds significantly over time.

Start with one action this week. A subscription audit produces immediate, measurable results in under an hour. A first monthly budget provides the structural foundation that makes every subsequent frugal strategy more effective. Either action moves you forward.